The One Change That Will Save Us $22,000

This blog post is part of the Pay Down My Debt (PDMD) blog tour, sponsored by US Equity Advantage. PDMD is a solution that accelerates debt payoff and helps consumers monitor their credit and make smarter purchasing decisions. If you’re looking to pay off debt find out how they can help.

I still have a hard time comprehending how far we’ve come since being in over $75,000 of debt back in 2008. In the midst of the huge financial crisis and recession, my wife and I found ourselves looking for ways to get out of the debt that I racked up while starting/running a business. One that I eventually shut down for my own well-being.

It’s going on 5 years this July that we paid off the last credit card and the massive pile of debt was lifted off our shoulders. The four years it took to pay down the debt was tough. It was grueling. It took a lot of sacrifice on our part.

A lot of discipline.

No matter who you are, paying down debt takes work. There is no magic bullet. Heck, not even bankruptcy is that magic bullet (and one I would never recommend to anyone unless it was a last resort). When it came to our debt, I looked to see if there were better options for us to pay down the debt faster and keep more money in our pocket. For our circumstance, I found the debt avalanche did better for us mathematically than the snowball. In the end, I’m glad I went with that method. It saved us over $5,000 in interest payments to the bank. Little victory!

Don’t forget that changing your financial outcome requires a lot of change. You need to learn how to make more money, save more, start investing, and continue to pay off debt. These are the aspects of money that we can control the most. These and understanding wants versus needs.

Now that we’re out of that debt hole, we are working on tackling just one more…

Our Last Debt on the Books

Some people have asked me if I included our mortgage in the $75,000 we paid off. The answer is no. I wish I had a mortgage for that low.

We bought our first house right before the market crash, but luckily I was smart enough to not accept what the bank “thought” we could afford. We went with a payment we could manage on our salary and it worked for us. When houses around us were going into foreclosure, we stayed put and made all our payments.

We stayed in our first house for 7 years and most of those were waiting for the financial crisis and housing market to stabilize. We wanted to get out of the area, have kids, and be in a better school district. In order to do that, we needed to sell. We ended up timing it just right and sold our house quickly.

Our current house was purchased back in 2014 with more than 20% down and we love it. We really do. Having said that, the mortgage debt is looming over our heads. We can easily afford the payment each month, but after going through four years of aggressively paying down debt, the mortgage just stayed there.

Now, it’s the last debt we have on the books and it’s time to tackle it head on.

Good thing is I have a little trick to save us some money over the life of the loan and it’s something everyone can do.

How We’re Slashing $22,000 Off Our Mortgage Interest

OK, as you can see, it’s not really $22,000, but that’s such a cleaner way than doing $21,885.46. But, how are we going this?

Bi-weekly payments baby!

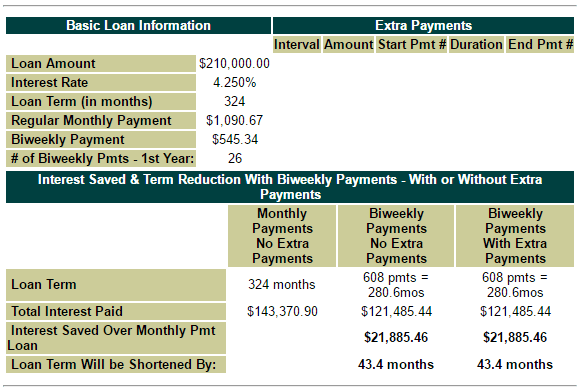

As you can see, we have $210,000 left on our mortgage at a 4.25% interest rate. For the past three years, we’ve just made the regular monthly payments as we had focus on building out our basement and using cash to build my business. We’ve been successful in both of those areas, so now it’s time to get laser focused on the mortgage.

Before I go on, there are some people that say you should not pay off your mortgage due to the low interest rate compared to investing. Invest for retirement first, then pay down debt. I don’t agree with that. I say do both!

OK, so back to our plan here. We are using a little trick that is called bi-weekly payments.

Instead of just making one payment per month, you end up making a payment every two weeks. These payments are your monthly payment divided by two. Over the course of the year, you end up making two extra half payments. This accounts to one extra full monthly payment per year.

Now, how does this save so much money? Wouldn’t you rather keep $22,000 instead of giving it away to the bank? I know I would.

Bi-weekly payments has a benefit because it shortens our mortgage loan (in our case it shortens it by nearly 4 years), but due to how interest is calculated on mortgage loans, the bi-weekly payments help cut it down.

It’s really a win-win situation here and one I plan on implementing very shortly.

You see, it’s not always complicated to save more money when you’re dealing with debt. Sometimes you just have to look for more efficient ways to pay down debt and the bi-weekly payments are just one way to do that.

How to Setup Bi-Weekly Payments

There are a few ways you can setup bi-weekly payments and the best part is this method works for really any debt. It’s not just for your mortgage! You can really apply bi-weekly payments to almost any loan, even credit cards.

The first step is to check with your loan servicing company (where you make your payments) to see if they allow or accept bi-weekly payments. Some will charge you a fee to do this, but generally the fee is quite small compared to the overall savings. So, check before you do anything.

If the company holding your debt allows for bi-weekly payments, ask if they have a system setup for it. Can you just set automatic payments every two weeks or do you have to create a schedule?

What if your bank/loan servicing company doesn’t provide you with a way to make accelerated payments? No problem, there is a service for that.

Pay Down My Debt is an accelerated debt payment service that helps you setup bi-weekly/bi-monthly payments to help you pay down your debts. You can pay down mortgages, car loans, student loans, or even high-interest credit cards with this program. The caveat is they charge $9.99 per month. While you might not want to pay that fee, just think how much you can save by using a service like this?

If I were to setup my mortgage through PDMD, I would pay a $3,240 over the course of the mortgage, but doing so would save me nearly $22,000. That’s a net savings of nearly $19,000. I’ll take those wins any day.

If I were to setup my mortgage through PDMD, I would pay a $3,240 over the course of the mortgage, but doing so would save me nearly $22,000. That’s a net savings of nearly $19,000. I’ll take those wins any day.

You might be asking yourself why would someone pay for a service that they could probably do for free?

Simple answer, habits.

We are creature of habit and when it comes to changing up our thinking and sticking with a plan that is long term, it becomes very hard to stay on track. I’m not saying that you can’t setup a bi-weekly payment schedule of your own and slay those interest payments, but most people won’t stick with the plan long term or even actually follow through with it.

If you have the discipline, then do it (that’s what my plan is), but if you know you might not keep up with the new payment schedule, then a paid service like Pay Down My Debt could be a good alternative.

You have to do what’s best for you.

So, there you have it. With just switching up our payment schedule from monthly to bi-weekly, we are going to save nearly $22,000 on mortgage interest and save nearly 4 years off the life of the loan. If we add any extra principle payments, we’ll drop it even more.

Bi-weekly payments are the easiest way to shorten your mortgage and save a ton on interest with barely noticing the results. Good on you for going that route. Good luck on making a few nice lump sum payments to save even more! I up’d my biweekly payments a few years ago and took my mortgage lifecycle down even more on one of my properties, it’ll be paid off in no time

Yeah, I might add a few extra dollars on top each bi-weekly payment to speed it up!

Awesome info. We wen’t a different route. Earlier this year we modified our loan from a 30 year (With just under 20 years left) at 6.75% to a 15 year at 4.25%. The savings on interest will be almost $90K if we pay out the full 15 years.

Modify a mortgage. I’d never heard about it until I called the bank to talk about refinancing.

It was easy. Sign one document. No appraisal, no survey, no points, just a $185.00 processing fee.

We even reduced our monthly payment by almost $100.00.

Definitely want to pay the house off early, so I’m looking into options. Glad I found your article, as I’m going to see what it will do for us.