Mint vs. Personal Capital – The Ultimate Financial Tool Throwdown

It’s here my financial friends. The ultimate throwdown! Today, we pit two of the best financial tools against each other to see who comes out on top. That’s right, we are going to compare Mint.com and Personal Capital to see which free tool is better! I got this idea back when someone basically asked me: “Mint.com vs Personal Capital?” Now, this is highly subjective as it’s my opinion on the matter. I plan on comparing the features of each service and see which one wins. There will be several categories.

We could see Mint winning or Personal Capital taking it. Who knows, but no matter what happens, let’s just say both of these tools are great. I have used both of them. Mint.com helped me get out of debt and Personal Capital has helped me grow my wealth. I would recommend any of them to anyone. The best part is they are both free! Yep, you can use both of them for free! Now, onto the best financial battle of late!

Let the games begin!!

Mint.com vs Personal Capital

The battle will consist of several categories that are most important to those who use these services. Since both services are free to use, it makes it much easier to compare. We won’t have to compare costs as there aren’t any! I will say that Personal Capital does have a management service for investments, but you are not obligated to use them in order to use their free platform. I just want to make that clear. We will focus on the following areas to make sure you understand the platforms and which one will work best for you. They include security, sign up process, interface, features, and mobile.

Sign Up Process

As mentioned, both accounts are free to sign up. That being said, free comes with some stipulations. While they are both free, they do require you to provide log in information for your bank accounts, credit cards, mortgages, investments, and whatever financial accounts you want to track. That being said signing up for either service is incredibly easy.

Personal Capital requires just three pieces of information in order to sign up. You need an email address, a strong password, and your mobile number. Why the mobile number? This is part of their security, which I will talk about later, but it’s simply to verify your account and the device you’re signing up on.

Mint.com requires similar information when signing up. They require an email address (have to enter it twice), your country, zip code, and strong password (entered twice). You also have to click a checkbox on Mint saying you agree to their terms and conditions. Once you do that, then you are ready to go!

Both services say that when you sign up, you are agreeing to their terms and conditions. Links are provided to their terms and policies to allow you to read them before signing up. I would recommend doing so. Personal Capital adds that when you sign up, you are agreeing to receive updates, offers and promotions from them. Mint.com has the same thing in their terms, but just don’t put it on the sign up page. You have to dig through the terms document.

*winner by the slightest of margins. The only reason for this is their device verification during registration. I like that and think other services should do it.

Security

This is one of the most important fights between these two service providers. People don’t like giving away the keys to their financial lives. I don’t either. I was skeptical of using either service some years ago. I didn’t really understand how they worked. Security is important to me and I think both services do a fine job handling their products. I’ll start with how Personal Capital works first, then move to Mint.com.

Based on the information from Personal Capital, they offer bank-level security alongside two-factor authentication. Here is what they say about data security on their site:

You create a single username and password to securely access Personal Capital’s dashboard and apps. You then enter usernames and passwords for each financial account you link to our system. Your credentials are encrypted in transit and at rest, using standards that are equal or better to than what is used at top-tier financial service companies.

No individual at Personal Capital has access to any client credentials. Our system is designed such that not a single employee could pull them even if they tried. All your usernames and passwords are encrypted from your browser or your mobile app to our systems, and remain encrypted when stored. Because no individual has access to this information, and it’s encrypted whether in motion or at rest, it protects your credentials from unauthorized access or use.

Here are the bullet points about what they provide you in regards to security:

- Two-factor authentication – You have to verify each device you use to log in. This is the same as using a debit card and you pin at the ATM. Someone would need both in order to get access to your account. Remember, your account is safer when you have a nice, strong password.

- Data Encryption – Personal Capital encrypts your data and login information with military-grade encryption. They currently use 256-bit AES, which is secure.

- Firewall/Perimeter Security – Since they have your data stored inside a data center, they need it to be protected. They have monitoring and data security standards which are set to the highest level for financial information. They have PCI (DSS Level 1) compliance and ISO 27001 certification.

- Continuous Monitoring – Along with their monitoring, they allow you do to it as well. If you want, they will send you a run-down of your financial transactions for the last 24 hours, every morning. You can then look to make sure all the transactions are truly yours.

One thing I like about PC is they call your phone when you try to log in with a new computer. You have to then approve it and they will move you to the next page. It’s pretty sweet.

OK, let’s move onto Mint.com and their security standards.

Mint.com uses 128-bit SSL security to encrypt your data when you enter it on their website. They also use the same physical security standards at your typical bank. Their site and processes are monitored by some third-party agencies such as TRUSTe and Verisign, including some others they don’t mention. Mint also provides you to create a four-digit pin when you are accessing your account on your mobile device. This allows you to keep your info secure if you were to lose it. They also provide you with a way to wipe the data on your phone if it were lost or stolen.

Mint doesn’t provide as much detail into their security practices as Personal Capital does. They just have a generic rundown of what they provide to each account holder. They are owned by Intuit, which is the maker of many products such as TurboTax. If you have an Intuit account, then you can easily sign into a new Mint.com account as they are together. As with PC, Mint.com advises you use a strong password, mixed up with letters, numbers, and symbols.

With regards to both services, many people have the common misconception that they not only have access to your bank information, but they can change amounts, categorizations, and other things. This is false. Both Mint and Personal Capital use what is called “read only” to just capture the information in your financial accounts.

You, and no one else, can change transactions, move money around, take money out, or anything else. What you do in your Mint or PC accounts are independent to what you will see when you log into your bank accounts.

* I give Personal Capital the edge due to their 256-bit encryption and two-factor authentication when signing up. They also don’t allow you to enter both your email and password on the same screen when using a browser. You can include both with Mint.com. This may irritate some users, but it’s a little added security measure

Interface

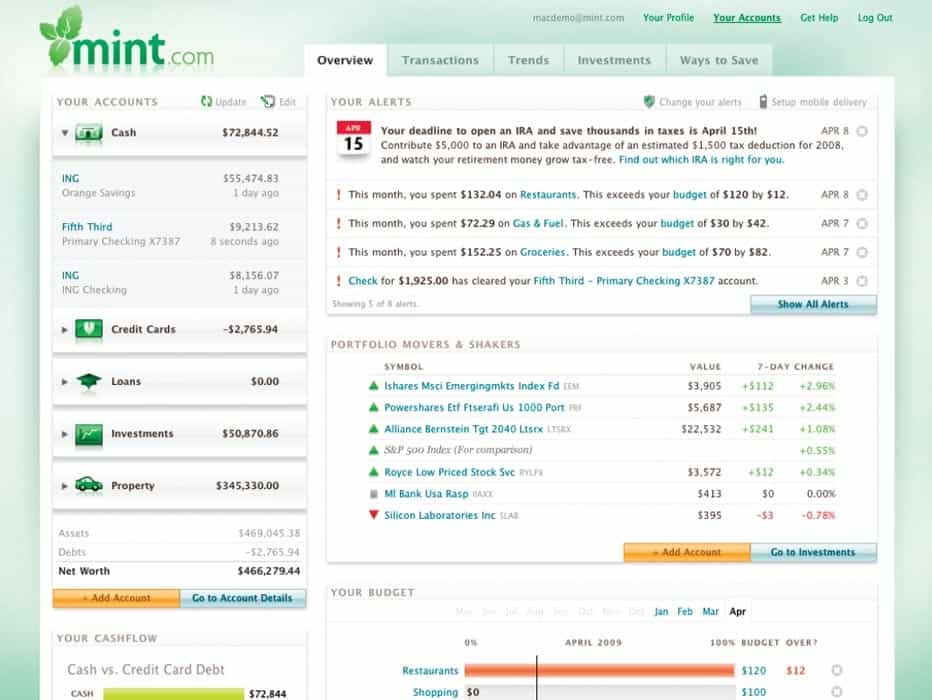

This one is obviously subjective. Both services have attractive interfaces, but it all depends on what you like to see when you log in. First, let’s start with Mint.com. Here is a snapshot of their dashboard.

When you first log into Mint.com, it takes it a little bit to sync up your financial accounts. It needs to bring in the most up to date information to be relevant. While it’s doing that, you can view your overall financial picture. One thing that Mint does well is their “Alerts” section right at the top of the dashboard. This area shows the important parts of your finances. Did a check just clear? Have you spend too much in once budget category? Are are spending too much overall? These can be very helpful.

Mint.com will also provide advice below your alerts. They have multiple advice pieces depending on your finances. Below that, you will see upcoming bills, which is nice way to visually see when your bills are due. Below bills, you will see your monthly budget and how well your spending is within each budget category. Mint allows you to setup goals, so if you have done that, you can see them on your dashboard. Below everything, you will see your investment movers and shakers, along with Mint’s “Ways to Save” area.

On the left-hand side, you will see all of your accounts and their sync status. Once they are all done, you will see how much cash you have on hand, how much debt you have, any loans, mortgages, autos, and all that jazz. It will then give you a run down of your net worth.

Under that, you will see how well your doing when comparing to your available cash compared to your credit card debt. Above everything there is a menu which allows you to see your overview page, which is the dashboard. You can also see your transactions, budgets, goals, trends, investments, and ways to save.

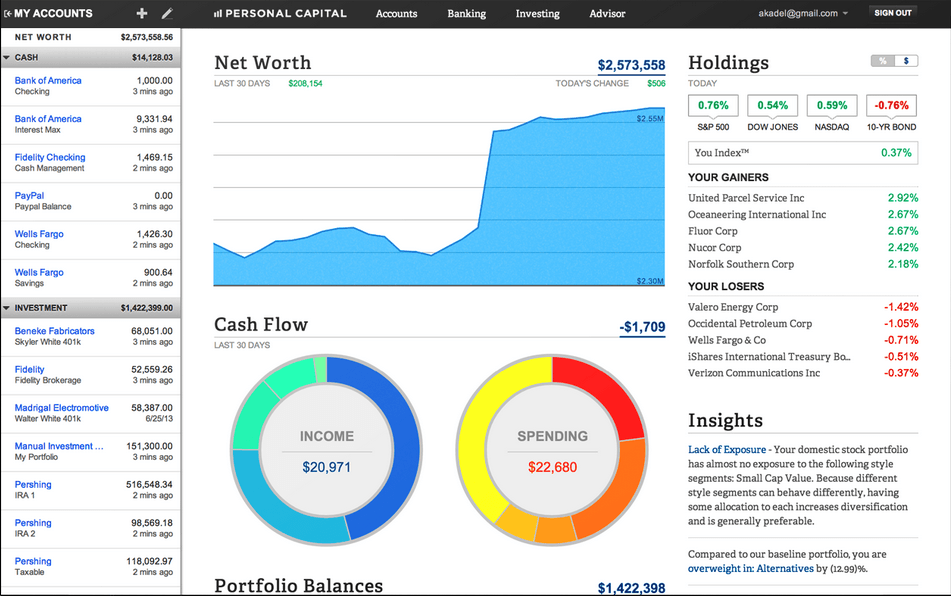

OK, now let’s shift to Personal Capital. For those who think Mint has too much stuff going on in their dashboard, then you will love Personal Capital. Here is what you will see when you log in.

Front and center in Personal Capital is your overall net worth and a graph that shows it’s ups and downs over the last 30 days. For people like me, this information is great. I like to see my net worth right in my face. Personal Capital keeps their dashboard relatively clean. They have your financial accounts loaded on the left-hand side of the screen. In the center, you see net worth, cash flow, portfolio balances, and portfolio allocations. On the right-hand side of the screen, you will see your investment holdings.

At the top of the page, you will tabs for accounts, banking, investing, and advisor. Most people are only concerned with accounts, banking and investing. Here you can see your net worth, transactions, 30 days cash flow, and your upcoming bills. The investing section will dive deep into your investment accounts and help you analyze where you are going wrong and what you’re doing right.

It’s hard to come up with a winner here. For me, I like the simplicity of Personal Capital, but Mint does a great job with their alert notifications. Since these two are so close, yet so different, I’m not sure I can provide a winner. It’s too subjective. OK, I will anyway!

[thrive_text_block color=”light” headline=”Winner”]

![]() [/thrive_text_block]

[/thrive_text_block]

*Mint wins this one with the smallest of margins. The only reason is they do provide a wealth of knowledge in their dashboards. You can make actionable changes based on goals, budgets, and bills.

Features

OK, what good are these services if they don’t provide you with some features. Now, I will disclose that though they both are free services, they can provide an overwhelming amount of information to you. I will also say that they both provide good features for anyone looking to get a bigger picture of their finances. Where they differ is in the core of their service. Mint.com is great for those looking to budget their money and keep to some goals. Personal Capital on the other hand is focused on retirement. For this reason, I recommend Mint.com for those looking to fight debt and Personal Capital for those looking to grow their wealth.

OK, let’s discuss the features which are similar between the two services, then we will look at where they’re different.

- Financial account aggregation – Both services allow you to add your financial accounts in order to get a picture of your money.

- Security features – Both offers enhanced security and read-only access to your financials. You can change stuff in both systems, but they won’t change them at the actual holder of said account. You can easily search for your financial accounts. You enter your log in information once and both systems will do the rest. You might have to answer your bank’s security questions from within their systems, but that’s only if they are used. Neither system has all of the banks, credit card providers, mortgage lenders, or any other financial account. There will be some smaller financial institutions missing from both.

- Banking transactions – They each pull in your banking transactions and put them in an easy to see area. This enables you to see what you’re spending your money on and how much each month you spend.

- Automatic Categorization – Each service uses algorithms to categorize your financial transactions. Most are pretty easy to get, but they sometimes get messed up. This is especially the case when a merchant doesn’t provide good descriptions to the banks. Other reasons are for when you pay with checks. They can’t accurately know what a check is for. Luckily, both systems allow you to change the category of each transaction. This helps you put them in the right place. Mint does allow you to create your own categories, but I don’t believe Personal Capital has such a service.

- Net Worth – Your net worth is something you should follow. It’s important to know where you stand financially and your net worth is a picture of your financial health. You can have a lot of cash or savings, but if your have too much in debt, then your net worth is negative. I’ve had a negative net worth, so I know how important it is to push that number to the positive area!

- Bill Monitoring – You can easily see when your bills are due in each system. Mint allows you to create notifications about your bills, but Personal Capital does not. You can mark your bills paid in PC, but you can’t in Mint.

- Cash flow – It’s really good to know how well your cash flow is doing. This is basically the difference between your spending and your income. Both services offer insight into this, but one uses a pie chart and another uses line graphs. Either way, you get a visual into how you’re doing with your spending!

Alright, now it’s time to see where these two services differ. Now, since they are very similar, I will show you three areas where they are different.

Budgeting – Mint.com is the clear winner when it comes to budgeting. They offer the easiest way to start budgeting. Don’t trust me? Try it for yourself. I used Mint.com when I wanted to understand where my finances had turned sour. It was incredibly easy to use and figure out. It can also change based on your projections. If budgeting is your need, then Mint.com is there to fulfill it. Personal Capital does not provide budgeting advice. On top of budgeting, Mint allows you to create goals for yourself. You can pay off debt, save $x, or whatever. The goals are based around the information in your Mint account.

**Update – Personal Capital has just created a budgeting section for their service. It’s only currently available for iPhone and iWatch users, but will soon be released on desktop and Android.

Investing – This is where Personal Capital’s bread and butter lies. They are an investment advisor service. They built their interface to deal with investments. If you have investments and want to know more about them, then PC is your service. They also give you access to a financial advisor, free with every account! While Mint does show investments, you get a wealth of knowledge from Personal Capital. Mint.com can’t touch PC in the investment space.

Advertising – Here’s the rub about these two services. They are free for a reason. Why though? Well, here is where it all comes together. Mint.com is able to provide this service because they have so many “offerings” or advertising on their site. They don’t go out of their way to use flashy banners, but they disguise their ads into their “advice” and “ways to save” section.

When you apply for a credit card through Mint to save on interest, they get paid. When you open an IRA account to funnel money into before taxes, they get paid. Most, if not all, of their advice is pushing paid partners. While I don’t mind it because I know the model, please know this is why it’s free. I stopped using Mint for the most part due to the overwhelming suggestions and emails about new services.

Personal Capital doesn’t provide any ads on their site. The model they use is based on your investments. Since they are investment advisor, they make money when they sign you up for their advising service. They look for those who have $25,000 or more in assets which can be invested. While they provide their service for free, they use the accounts in their system to look for potential clients. They currently manage over $1 billion in assets, so they know what they’re doing. One of the reasons I like Personal Capital is their dashboard is ad-free and it doesn’t clutter up what I’m trying to look for. I just get clear/concise information when I need it.

*I can’t declare a winner here, because it depends on what you want from the service. They both have a similar core set of features, but Mint.com does a better job with budgeting and goals. Personal Capital wins when it comes to investments.

Mobile

We are a country of smartphone addicts, that’s for sure! If you can show me a place where people aren’t tapping away at their screens, I would be impressed! Maybe church, but I’ve seen it there too. Since we love our smartphones, these two services wouldn’t be complete without a smartphone app!

Both Mint and Personal Capital have mobile apps for both Android and Apple. Here are Mint’s Android and Apple apps. Here are Personal Capital’s Android and iPhone apps. If you just look at the reviews, you will see that Personal Capital has slightly better reviews overall, but they also have a smaller quantity, so take it with a grain of salt. Let’s discuss Personal Capital’s mobile experience. I’m using an Android phone, so just want to make that clear.

Personal Capital’s app is clean and easy to use. When you first download the app, you will need to enter your account email. You can also sign up through there. Once you sign up, you will need to verify the new device. They will either call you or email you. You decide. Once you verify the new device, you need to enter your password. Go to the next step and you will enter a six-digit pin number twice. If it’s your first time, then you create this pin. This pin allows you access to your account. Without it, you don’t get in. This allows you to control your account, in the event your phone is lost or stolen.

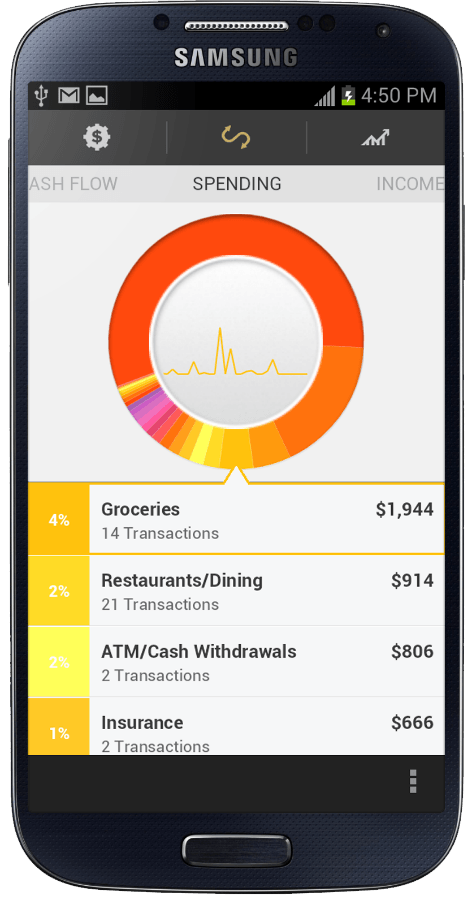

When you log in, you are greeted with a simple dashboard showing your net worth. You can scroll down to see your transactions, cash flow, and investments. When you scroll down, the graphs change depending on what section your in. They default to the last 30 days, but you can change those in the settings. If you want to look into different things in detail, you need to click on the Personal Capital logo at the top of the app and a menu will drop down. You can then go to each section, like they have on the site. It’s simple to use and does the job. Nothing fancy, but a very well-rounded mobile app.

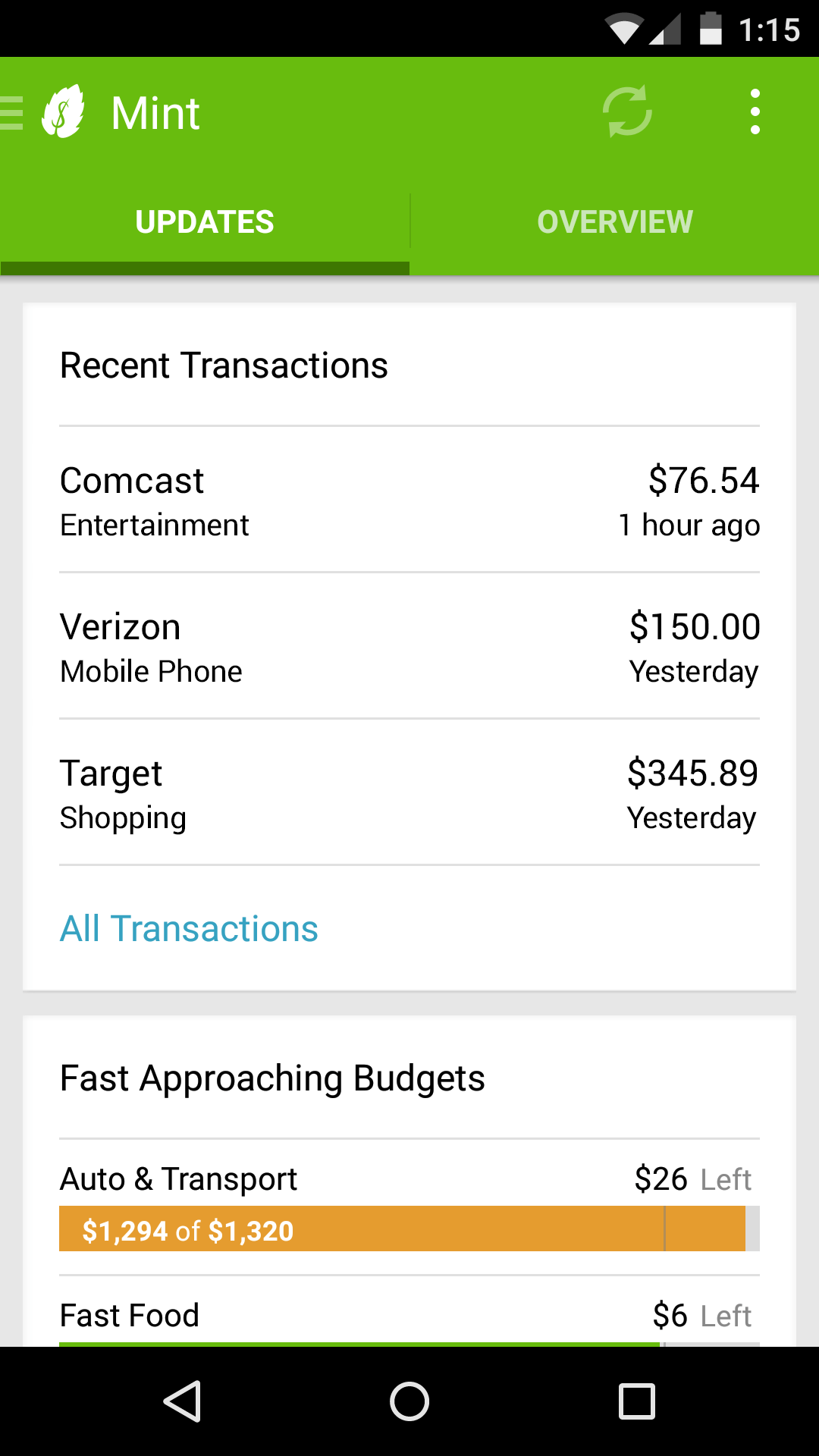

Mint.com also has a good app to use. When you download the app, they allow you to sign in with your username and password. Then they download your transactions. You first arrive on the Updates tab, where you see your latest and greatest when it comes to your finances. What you paid last, some transactions, the last bank account you used. You can also hit the overview tab, which is a nice run down all all things Mint.com. They show you similar things on the mobile app as they do on their website.

One thing I don’t like about Mint’s mobile app is their updates section is full of offers/advice/ways to save. As I mentioned, I’m not a fan of these things. I realize Mint makes money from these and that’s how their model works. On the flip side, one aspect of Mint’s app, which I like is you can enter manual transactions into your account. It’s simple and effective. This is really important if you do a lot of cash transactions.

Mint.com does tell you that you should setup a pin in order to secure your mobile account. I was under the impression they would force you to do so, but they don’t. You have to go into the setting and set it up. Personal Capital forces you to create a six-digit pin, while Mint just suggests a four-digit pin. As with PC, Mint also allows you to dig deeper into specific areas of your finances by clicking on the Mint logo. A menu appears and you are off and ready.

*There is a caveat here. Both mobile apps are clean and effective. The edge goes to Personal Capital due to them forcing you to create a six-digit passcode in order to log in. I like that feature, while Mint’s was just a suggestion. I also don’t want my dashboard cluttered up with advice/ways to save in order to get Mint their cut.

Mint.com vs Personal Capital – Who Wins?

What a grueling battle. If you stayed throughout this extremely large and in-depth post, then I congratulate you! These are the two services that are most often talked about, so I wanted to put them up against each other. Remember, this is highly subjective based on my experiences with both services.

I do currently have both active and log into them regularly. For me in my current financial stage, Personal Capital is the winner. While Mint.com has great budgeting applications, I’m interested in investing right now and growing my wealth. Personal Capital has changed my financial life due to the investment checkup tools and everything else they provide based on investing. Most of us won’t reach retirement with enough money if we don’t invest.

This is why I’m focusing on it now. I’ve paid off my credit card debt and moved on. Mint had it’s place, but now it doesn’t fit what I need it to do. I still have it in order to make sure we are on budget with our spending. Since Personal Capital doesn’t really offer budgeting, Mint still is around for that.

As I noted, this was an extremely close battle. Both services offer great insight into anyone’s finances. It really all depends on what you want to do with your money and where you’re at in life. No one can tell you which software to use, but I use and recommend both of them. Right now, Personal Capital is more up my alley and does the job I need it to do. So…

Alright, let me explain why I gave the win to Personal Capital. While I focus on investing, I’m not really worried about my investments on a daily basis, but I do care about my fees. Personal Capital helped me reduce my fees and diversify a little more based on what my accounts where holding. This was extremely useful for me. I’ve stayed with PC because their interface is so clean. They don’t bog me down with a bunch of offers I don’t care about. They also only email me once a week with a nice snapshot of my investments, my spending, and all the information I need. Mint.com has it’s place for many people, but I prefer Personal Capital for it’s security, lack of advertising, and clean interface. The other major factor was accounts having trouble connecting inside Mint.com. I consistently had issues with some accounts dropping sync in Mint. I’ve never had such problems in Personal Capital. Mint also wouldn’t connect to my 401k provider, but Personal Capital did with no problem. That’s a big chunk of my money, so I need to be able to see it.

You can learn more about Mint.com here and Personal Capital here.

Alright, that was a long financial battle. The key two both of these services is you being able to load in your financial accounts. Mint has been around for a long time and they helped me get out of debt with their budgeting tools. I’ve since moved on as Personal Capital has changed my financial life because it opened my eyes to my investments, something I didn’t focus much on when I was younger (stupid!). No matter what one you choose, just pick one!

Most images were provided by Mint.com or Personal Capital for this financial tool battle.

I haven’t tried either yet but am thinking about going with Personal Capital. I like their added security measures, and I think the interface looks like a cleaner, clearer picture of the accounts. Great and thorough post, Grayson!

I think you will like Personal Capital Laurie! They are great and much cleaner interface than Mint.com.

This is a great comparison. I don’t personally use either because I like the program that I use for my clients, so I use it personally as well. However, I have people ask me all the time about what I would recommend and I personally like personal capital’s interface better than mint. At the end of the day, I think all that matters is that you use something to track your money.

Well, if you have a program you enjoy, then go with it! You’re right. At the end of the day, as long as you track your money, then it doesn’t matter. I think these two services provide a value to many people.

Grayson thanks very much for the detailed comparison! I’m a long time user of Mint and have been larger happy with everything related to my banking and budget tracking. As I begin to get deeper into investing and caring more about my retirement savings (and associated fees) I’ve been hesitant to try PC. Based on your review it definitely sounds like something that will benefit me. Thanks Again!

Hey Dan,

I was a user of Mint for over six years before I found Personal Capital. Now, I still have my Mint.com account, but rarely log into it. My Personal Capital account is my go-to because I like the interface much more.

This is a thorough terrific write up! I used Mint for years sporadically. The budget section just was a lot of work and I didn’t keep up with it like I should but found it easy to sign into one place to get all acct info.

The other annoyance like you mentioned were the ads disguised as advice every time I signed in. I know it’s free but come on now!

So after reading a brief review from another site I took the plunge with Personal Capital and am in love! Very simple and clean app. Wicked easy to sign up my accts, and I sign in almost daily. Since I am in debt war, I love watching and monitoring all the happenings from increased 401 contributions to paying down credit cards. It updates in real time. Plus the monitoring of spending habits is just right and easy to analyze. I prefer a pen and paper budget anyways.

Thanks for the comment Dawn! You’re right on what you say. PC is very clean and non-cluttered. You can get the information you need whenever you log in. You don’t have to wade through the “ads” like on Mint. It’s one of the main reasons why PC is my preferred service.

Interesting review. It’s great to see them go “head to head” so to speak. They both seem to have some great features and each has pros and cons. Thanks for all the details.

I thought going “head to head” would make it more informational for those looking between the two services. Since they’re both free, you really need to know what you’re looking for.

I’ve used Mint for quite a while now and use it primarily for the budgeting function. What ever app you choose is a personal choice, the most important thing is that it results in the user being able to better manage their finances.

Mint has a better budgeting function, but Personal Capital just added it to their iPhone app. I’m interested to see how it works. You are correct, whatever someone chooses, just make sure it actually helps you!

Nice review Gray. I have been a user of Mint for several months now and I can say that it has helped me out so well with my budgeting. I think I gotta try Capital Service, which I have heard so many good reviews. It feels great to have a reliable app to assist us especially with budgeting, savings, and finances. Thanks for doing this because it helps me with my decision. More of this to come, Grayson!

Great review Grayson. I’ve tried Mint out before and was impressed with how easy to use the web interface was. I was not a huge fan of their mobile app, it felt clunky and slow, and like you mentioned they try to shove offers down your throat.

I’ve never tried Personal Capital, but have heard good things from friends. Its a huge bonus that they don’t seem to have as many ads / offers as Mint.

Mint does have an easy to use interface, but they destroy the user experience with ads and offers in my opinion. That’s why I went with Personal Capital. They have zero ads in their interface and their mobile app is quick, responsive, and gives you the data you need.

Are you able to itemize credit card expense with either site to allot to spots in your budget?

You can in Mint, but I have’t tried the new budgeting tool in PC yet. It hasn’t been released on desktop.

Nice review Grayson. Many months ago, I considered utilizing Mint but couldn’t get over the thought of providing all of my account usernames and passwords. After reading several reviews, I am now convinced that my login info will not be compromised. Can you clarify two related and prevailing items for me? I will receive a state government pension upon retirement. Can either of these financial tools link to my pension account? Also, can either of these financial tools link to my state government provided 457 deferred compensation account? Thank you for your help.

Brian,

I wouldn’t be able to tell you if they could connect to our pension accounts or state deferred accounts. I would think Personal Capital could probably handle it better than Mint. I find they do better with obscure retirement/investment accounts than Mint.com does. You can always ask them. Personal Capital does have a neat retirement calculator that allows you to put in information regarding a pension to help you plan. The worst case is you sign up for Personal Capital and try to add both of those accounts first to see if they work. If not, then delete your account. It is free!

I’m a big personal capital fan – though it drives me crazy that it can’t sync up to my tradeking account!

What, no TradeKing sync? Did you reach out to them? I would think that should work.

I’m sure both websites can generate cleartext versions of all your passwords. The passwords are stored encrypted, but they must be converted to cleartext so the site can log on to the various banks and download your transactions. Some brokerages have a separate read-only password for downloading data. Let the User Beware.

Here is an explanation of how they use passwords at Mint for both logging into the platform and how they log into banking sites. Personal Capital uses similar processes…

“For passwords to Mint itself, we compute a secure hash of the user’s chosen password and store only the hash (the hash is also salted). Hashing is a one-way function and cannot be reversed. It is not possible to ever see or recover the password itself. When the user tries to login, we compute the hash of the password they are attempting to use and compare it to the hashed value on record. (This is a standard technique which every site should use).

For banking credentials, we generally must use reversible encryption for which we have special procedures and secure hardware kept in our secure and guarded datacenter. The decryption keys never leave the hardware device (which is built to destroy the key material if the tamper protection is attacked). This device will only decrypt after it is activated by a quorum of other keys, each of which is stored on a smartcard and also encrypted by a password known to only one person. Furthermore the device requires a time-limited cryptographically-signed permission token for each decryption. The system (which I designed and patented) also has facilities for secure remote auditing of each decryption.”

– David K Michaels, VP Engineering, Mint.com

Thanks Grayson for posting this explanation. I believe, however, it is missing the crucial step. Once the bank account password is decrypted using the special hardware above, it must be sent as plain text to the bank, probably across an SSL link. At this point, it can be intercepted by someone at the company. Admittedly, they would need access, but it’s not unheard of, and would bypass the encryption hardware/quorum etc described above. This can happen elsewhere too, for example, at the bank. I believe in the recent Ashley Madison hack, they passwords were discovered because they were logged before they were encrypted. In any case, the issue is whether to trust the developers of the website that all the crucial steps were done right.

I just gave the explanation from their engineer. I guess you’d have to trust any of these companies since even desktop applications do something similar where they interact with your bank. By your explanation, all of them would be susceptible to the same type of security flaw. You would need to reach out to Mint or Personal Capital for more information about it if you want to get on that type of technical level. I’m not an engineer and didn’t design the systems.

I just set up on Personal Capital this morning. So far . . . PROS: Clean interface; quite intuitive; connected easily to all but one mutual fund. CONS: Unable to add categories; unable to post a comment or post (kept getting looped into “sign in” prompt but when signed in took me back to home page.) Inability to create categories is a problem when you have unique needs – e.g., rental income, as a number of users noted.

Do you know if Mint allows adding categories? This may be a deal breaker for me.

I think you can edit categories on Mint.com.

Mint allows you to add custom subcategories. However, you can’t add to the top level categories which I listed below. It would be nice to be able to edit the top level categories and even add a third level. I suspect these limitations allow for better auto categorization of transactions.

Auto & Transport

Bills & Utilities

Business Services

Education

Entertainment

Fees & Charges

Financial

Food & Dining

Gifts & Donations

Health & Fitness

Home

Income

Investments

Kids

Loans

Misc Expenses

Personal Care

Pets

Shopping

Taxes

Transfer

Travel

Uncategorized

I like the clean-ness of Personal Capital, but there are some major problems they have. If you have a credit card account not on Personal Capital (like the Ally CashBack card), you can’t add those transactions manually, so technically, that spending never shows up on your categories of spending. Big CON in my book. (and anything labeled “credit card payment” in my bank account doesn’t show up in your spending in PC, so that money essentially “disappears” out of my budget).

In addition, the inability to split transactions and add subcategories for budgeting purposes really turns me off. I like having control, and when a program takes away the one thing I’d want, I am no longer interested in the program. I stopped using Mint a while back, but since budgeting and having more manual control are better with Mint, I’m going back.

I believe they are working on the budgeting aspect in their system. It’s supposed to already be live on iOS mobile, just not desktop yet. Good point though.

Nice review, but one thing you might call out is that both Mint and PC are “net” money management systems. In other words, neither of them have the ability to track your paycheck deductions. This is a severe limitation for anyone who needs reports that include deductions. For example, I need reports that show total spending for medical across the year. These tools have no way to do that. Unfortunately, the only ones I know of that can are either client-based tools (Banktivity) or are very ugly (Countabout) or buggy with a questionable future (Buxfer).

Yeah, I don’t run across too many who need to know that info or are looking for something that will track paycheck deductions. In fact, I think you’re the only one who has ever even mentioned they would need to know paycheck deductions in their money management system.

I too had been using Mint.com for years. I switched to PC today after stumbling across it. Mint was simply too busy and Ad-intrusive for my tastes. I prefer the simpler, cleaner interface and ease of use of PC over Mint.

Glad you found it. PC is much cleaner and doesn’t have the very annoying ads that are in Mint.

I have not used Mint.com in a long time, but just recently setup my accounts in Personal Capital. PC does allow you to create custom income/expense/transfer categories in their iOS app. Once you create custom categories in iOS, they become available in desktop and Android. I’d assume that they’ll eventually roll this functionality out in the other two.

Their budgeting section does leave something to be desired. I would like it if they allowed you to set individual budgets for different categories and alert when that was exceeded in a given month. Also another downside is budget only applies to expenses, not income.

Yeah, they have some ways to go with their budgeting app section. They know it and have been working on it, but I don’t have an ETA on when they will complete it.